.svg)

Global payments, untangled.

Multi-currency business accounts for cross-border companies - operated under Swiss AML regulation. Manage EUR, GBP, USD, and CHF accounts, execute payouts, and exchange currencies all under one compliant platform.

Trusted by 100+ cross-boarder businesses across different industries

Swiss-regulated infrastructure for global payments.

One account.

Multiple currencies.

Swiss reliability.

Manage EUR, GBP, USD, and CHF under one secure structure. Built for global businesses that need to send, receive, and exchange funds across borders with confidence.

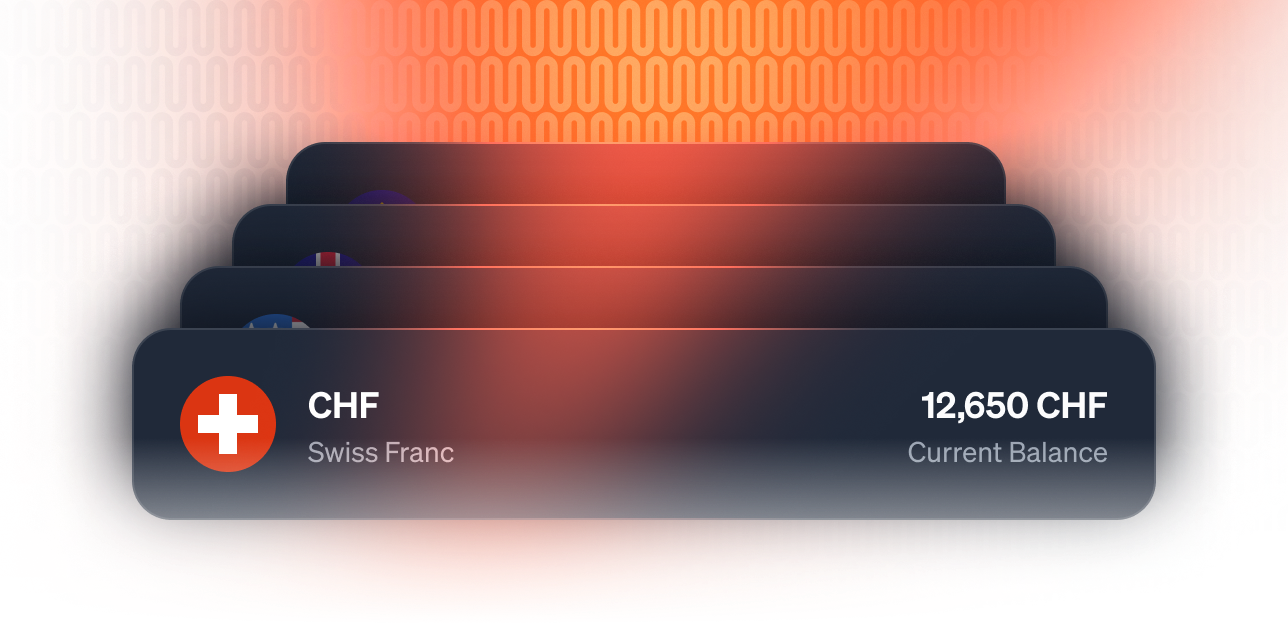

Business accounts in major global currencies

VQF SRO member · funds held with regulated partners

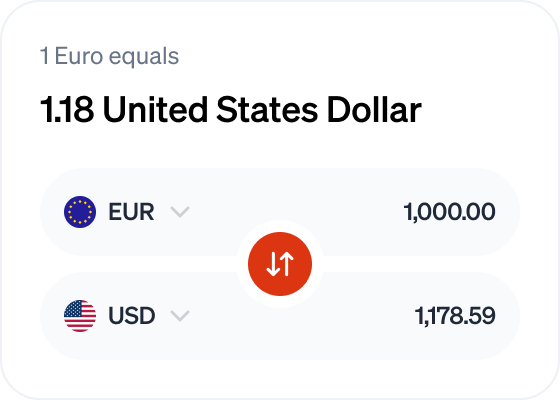

Transparent FX and cross-border execution

EUR

5,275 EUR

GBP

2,821 GBP

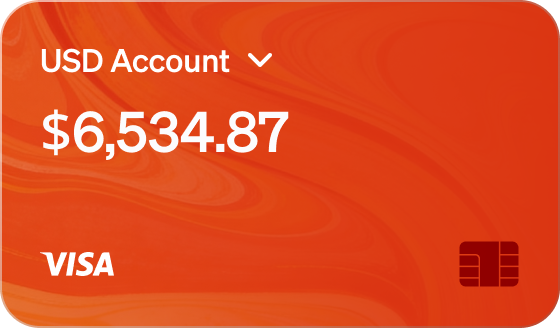

USD

2,821 USD

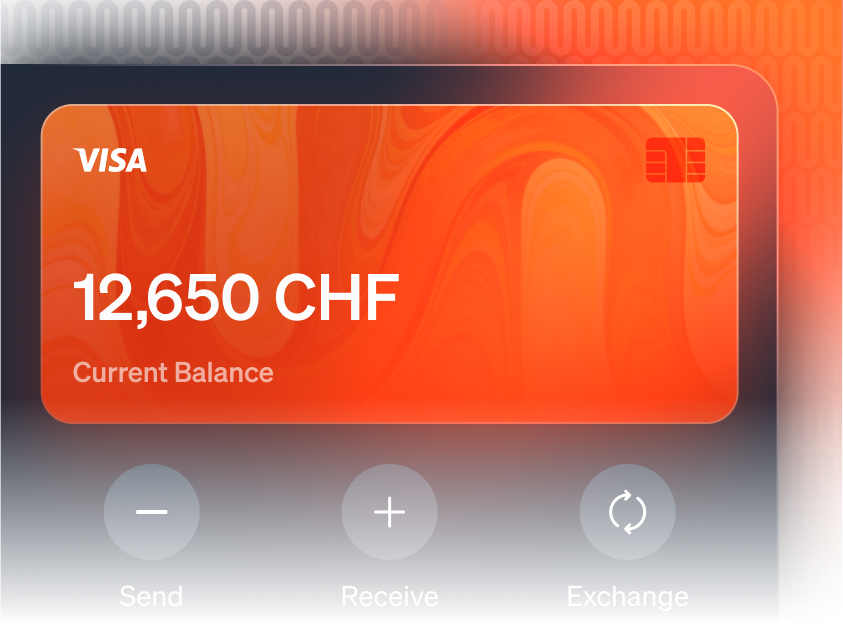

CHF

12,650 CHF

.png)

Register your business

Submit your company details, verify your directors and shareholders, and complete a short KYC/KYB process to activate your Nudl dashboard.

Connect or fund your account

Link your existing business bank account or add funds through our regulated partners.

Manage global payments and FX

Send, receive, and exchange major currencies directly from your Nudl web or mobile app.

Send money to 150+ countries with Nudl

.png)

.png)

.png)

Common questions

Find quick answers about Nudl’s business accounts, payments, and compliance framework.

Is NUDL regulated?

Yes. Nudl operates through Quixo AG, a member of the VQF Self-Regulatory Organisation (No. 101241), recognised by FINMA under the Swiss Anti-Money Laundering Act. This means Nudl follows Swiss AML and KYC requirements. Nudl is not a bank and does not hold a banking licence.

Is NUDL a bank?

No. NUDL is not a bank and does not hold a Swiss banking license. NUDL provides payment infrastructure and compliance services as a regulated financial intermediary.

Under which laws does NUDL operate?

NUDL operates under:

- Swiss Anti-Money Laundering Act (AMLA)

- Applicable Swiss financial intermediary regulations

- SRO rules and oversight

- International AML and counter-terrorist financing standards

Where are client funds held?

Client funds are held with regulated third-party financial institutions.

NUDL does not operate as a deposit-taking bank and does not use client funds for its own operational purposes. Funds are held with regulated third-party banking partners in accounts separate from Nudl's own assets. Nudl does not invest or lend client funds. Funds are not covered by Swiss deposit insurance.

Can NUDL use client funds?

Client funds are used solely for the purpose of executing payment transactions as instructed by clients.

NUDL does not invest, lend, or generate interest on client balances.

How can my business send or receive payments with Nudl?

Send and receive payments by funding your Nudl account via bank transfer or through our regulated banking partners. Payments are routed through Clear Junction, our licensed banking partner. All accounts are subject to KYC/KYB verification before activation.

How is my data protected?

Client data is stored within secure infrastructure environments aligned with Swiss data protection standards.

All identity verification processes are conducted through regulated third-party verification providers operating under strict compliance frameworks.

Does NUDL perform KYC and AML checks?

Yes. NUDL conducts identity verification (KYC/KYB), transaction monitoring, and ongoing compliance reviews in accordance with Swiss AML regulations and SRO requirements.

Enhanced due diligence is applied where risk classification requires it.

Who monitors compliance?

NUDL operates under SRO supervision and maintains independent compliance oversight functions.

AML controls, transaction monitoring thresholds, and risk classification processes are reviewed in accordance with Swiss regulatory standards.

Is NUDL a wallet provider?

NUDL provides payment execution and multi-currency transaction infrastructure.

Accounts are designed for operational payment flows and business transactions.

Does NUDL hold long-term deposits?

NUDL does not offer savings accounts or investment products. Funds are intended for transactional and payment purposes.

What happens in case of insolvency of NUDL?

Client funds are held with regulated third-party banking partners, separate from Nudl's own assets. In the event of Nudl's insolvency, those funds are not part of Nudl's estate. Funds are not covered by Swiss deposit insurance.

Are funds protected under Swiss depositor insurance?

No. NUDL is not a licensed bank, and Swiss depositor insurance (esisuisse) does not apply.

Does NUDL pay interest?

No. NUDL does not pay interest on client balances.

Can NUDL refuse a transaction?

Yes. As a regulated financial intermediary, NUDL may suspend or reject transactions that raise compliance, AML, sanctions, or regulatory concerns.

Download the App

Global payments, untangled.